Samsung and SK hynix Lead Korea’s 1,350 Trillion Won AI and Semiconductor Expansion

South Korea has unveiled one of the largest technology infrastructure programs in history, with Samsung Electronics, SK hynix, and other major companies preparing investments worth at least 1,350 trillion won, approximately 880 billion dollars, across semiconductor manufacturing and artificial intelligence data centers.

The headline figure combines 800 trillion won allocated to a new semiconductor production ecosystem in southwestern Korea with an initial 550 trillion won planned for AI data center construction. It should not be interpreted as a direct 1,350 trillion won fab investment by Samsung and SK hynix alone. The broader national strategy also includes physical artificial intelligence, robotics, advanced packaging, electricity infrastructure, water systems, workforce development, and regional industrial expansion.

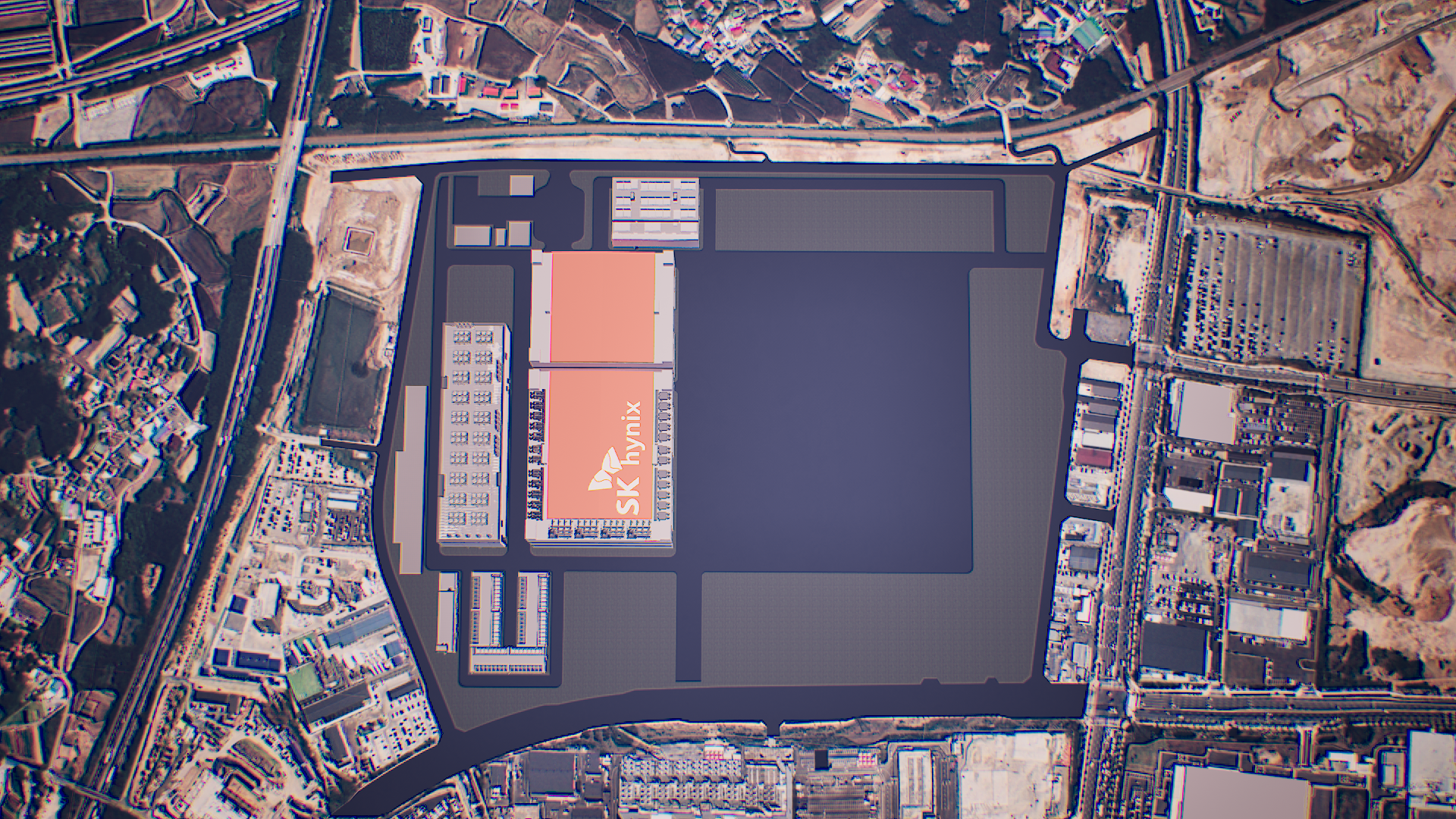

Samsung and SK hynix will each build 2 major semiconductor fabrication facilities in the southwest, creating 4 new fabs under an investment program valued at approximately 800 trillion won, or 518 billion dollars. Samsung has selected Gwangju for its new production cluster and plans to invest approximately 400 trillion won, while SK hynix has committed another 400 trillion won to a separate southwestern manufacturing base whose final location has not yet been announced.

The projects form part of South Korea’s effort to reduce the semiconductor industry’s heavy concentration around Seoul and establish additional manufacturing capacity in regions with greater access to land and underused electricity resources. President Lee Jae Myung argued that existing production centers around Yongin and Pyeongtaek are approaching their infrastructure limits.

“We must secure the core elements of AI faster than any other country.”

— Lee Jae Myung, President of South Korea

The government expects the new fabs and accelerated construction at existing sites to double national DRAM production capacity within 5 years. That expansion is intended to address rapidly increasing demand for conventional DRAM, server memory, NAND Flash, and high bandwidth memory used inside AI accelerators.

SK hynix is also accelerating development of its Yongin semiconductor cluster. The company now aims to complete the fourth Yongin fab by 2033, moving the target forward by 12 years from its previous 2045 schedule. The investment will be introduced according to market conditions and still requires individual board approvals as each construction stage advances.

A separate 100 trillion won SK hynix program will expand its Cheongju operations. Approximately 80 trillion won is expected to support the M17 NAND fabrication facility, while another 20 trillion won will fund the P&T7 advanced packaging plant. These facilities are expected to strengthen both NAND production and the packaging capacity required for increasingly complex AI memory products.

Samsung has outlined another 140 trillion won investment across the Chungcheong region. Samsung Electronics will spend 56 trillion won on high bandwidth memory production and packaging facilities in Cheonan and Onyang. Samsung Display will allocate 67 trillion won to display production, while Samsung SDI and Samsung Electro Mechanics will invest in batteries, semiconductor materials, and AI server packaging components.

The Chungcheong region will also receive approximately 81 trillion won for a wider semiconductor packaging cluster. This investment is separate from the 800 trillion won southwestern fab program and is intended to expand the supporting ecosystem required for high bandwidth memory, advanced logic packaging, materials, testing, and production equipment.

The scale of the expansion could intensify global competition for semiconductor manufacturing equipment. Samsung and SK hynix will require substantial numbers of lithography, etching, deposition, chemical mechanical polishing, inspection, photomask, and packaging systems as construction progresses. Industry sources cited by TrendForce warn that the program could tighten the availability of critical equipment also needed by TSMC and Intel for their own advanced process expansions.

That does not mean the investment will immediately weaken TSMC’s foundry leadership. Much of the announced Korean spending is concentrated on memory, high bandwidth memory, NAND, packaging, infrastructure, and data centers rather than direct competition in leading edge contract logic production. TSMC therefore remains better positioned in advanced foundry manufacturing, although Samsung could use the combination of memory, packaging, and foundry services to offer more complete AI chip production packages.

The AI data center portion of the plan is equally significant. SK Group, GS Group, Naver, and other companies are expected to invest approximately 550 trillion won in an initial 8.4 GW of computing capacity, with construction scheduled to begin by the first half of 2028. Total AI data center spending could exceed 1,000 trillion won by approximately 2035 if the later phases proceed.

This infrastructure will create additional demand for accelerators, server processors, networking, storage, cooling, electricity, and memory. SK hynix sampling 48 GB HBM4E at 16 Gbps, illustrating how the company is already preparing for future AI systems that require greater memory capacity, bandwidth, and power efficiency. The expansion could eventually provide relief for the current memory shortage, but new fabs will not improve availability immediately. Semiconductor facilities require years of construction, equipment installation, process qualification, yield improvement, and customer validation before reaching meaningful production volume.

SK hynix has already started rebalancing selected production resources toward DDR5 as conventional DRAM shortages push mainstream memory margins higher. However, server operators and large technology companies may absorb much of the additional supply through long term contracts before consumer memory pricing experiences substantial relief.

The plan also introduces considerable risk. Samsung and SK hynix shares declined after the announcement as investors considered the possibility that massive production growth could create oversupply if AI demand weakens before the new facilities reach full output. South Korea must also secure enough electricity, water, transportation, housing, and skilled workers to support production clusters located outside the country’s established semiconductor regions.

South Korea is not simply expanding semiconductor production. It is attempting to build a complete national AI supply chain connecting memory, advanced packaging, data centers, robotics, energy infrastructure, and manufacturing equipment.

The strategy reinforces Samsung and SK hynix where they are already strongest. Together, the companies control a dominant portion of the global memory market, while SK hynix leads in high bandwidth memory and Samsung combines memory production with foundry, packaging, displays, and consumer electronics.

The 1,350 trillion won figure nevertheless requires context. Only 800 trillion won is currently assigned to the southwestern semiconductor ecosystem, while 550 trillion won represents the first phase of a wider AI data center program involving additional companies. Many investments will also depend on future demand, infrastructure readiness, regulatory approvals, and corporate board decisions.

For consumers, the expansion is positive but offers no immediate solution to expensive DDR5, NAND, or graphics memory. The first meaningful supply impact will arrive years from now. For TSMC and Intel, the more immediate issue may be competition for equipment and engineering talent rather than direct loss of advanced foundry customers.

South Korea is making an enormous bet that AI demand will remain strong enough to justify this capacity through the next decade. If that demand continues, the country could strengthen its position at the center of the global computing industry. If the market slows, the same investment could produce one of the largest memory oversupply cycles the semiconductor sector has ever experienced.

Will South Korea’s massive expansion solve the global memory shortage, or could 4 new fabs create another major oversupply cycle later in the decade?