Intel’s EMIB Gains Momentum as a Potential Alternative to TSMC CoWoS in the AI Packaging Race

Intel’s advanced packaging business may be entering one of its most important growth windows yet, as rising pressure on TSMC’s CoWoS capacity pushes more customers to consider alternatives. A new report from DigiTimes says Intel’s EMIB is gaining traction as a fallback option for fabless chip designers, with the second half of 2026 shaping up as a possible turning point for the company’s packaging business. Even from the limited public preview of the report, the direction is clear: tighter CoWoS availability is forcing the market to look harder at Intel’s packaging stack.

That broader industry context matters. Advanced packaging has become one of the most important choke points in AI hardware because modern accelerators increasingly rely on multi die integration, high bandwidth memory, and more complex package level interconnects. TSMC remains the dominant player here, but Reuters reported earlier that advanced packaging has stayed a bottleneck even as TSMC rapidly expanded capacity for AI customers such as NVIDIA. In practical terms, that means customers are not only competing for wafers anymore. They are competing for package level assembly and integration capacity as well.

Intel’s opportunity is not just theoretical. At the Morgan Stanley Technology, Media and Telecom Conference on March 4, Intel CFO David Zinsner said customer engagement around EMIB and EMIB T has strengthened materially, adding that Intel is “close to closing some deals that are in the billions of dollars per year in terms of revenue.” The Register, which directly quoted the remarks, framed this as one of the clearest signs yet that Intel Foundry could generate meaningful external revenue from packaging rather than relying only on wafer manufacturing wins.

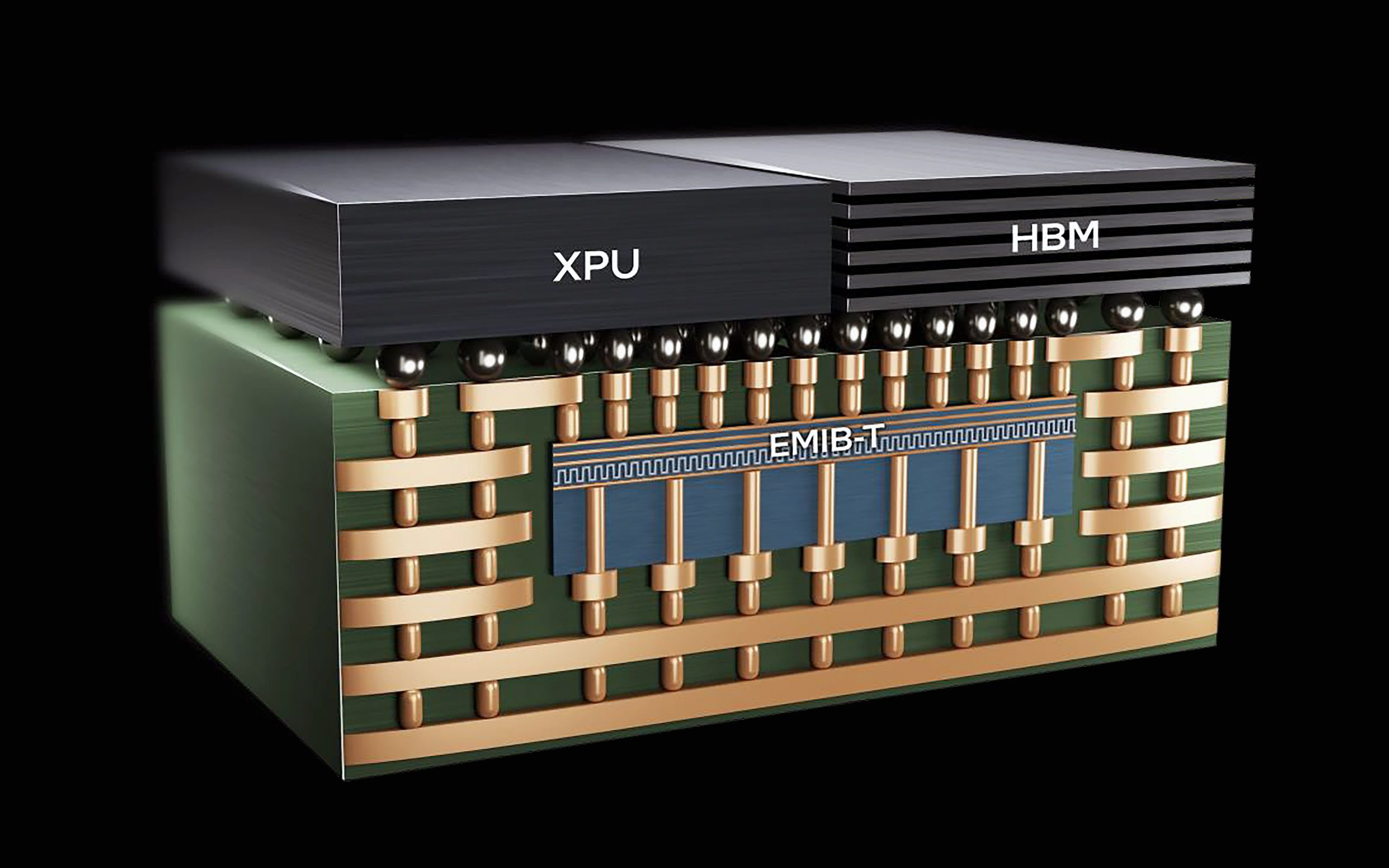

Technically, Intel is also positioning EMIB as more than a simple backup. Intel’s own foundry materials describe EMIB as a 2.5D packaging approach that embeds a silicon bridge directly into the package substrate, allowing dense die to die connections without requiring a full size silicon interposer. Intel says EMIB M adds MIM capacitors in the bridge, while EMIB T adds TSVs, giving the company more flexibility for logic to logic and logic to HBM style integration. That does not automatically make EMIB a direct one for one replacement for every CoWoS design, but it does explain why customers looking for cost, scale, or design flexibility may find it increasingly attractive.

The US manufacturing angle also strengthens Intel’s case. Intel officially opened Fab 9 in Rio Rancho, New Mexico in 2024 as part of a 3.5 billion dollar investment focused on advanced packaging technologies. That gives Intel real domestic advanced packaging infrastructure today, while TSMC’s Arizona expansion includes future advanced packaging plans but is still part of a broader buildout timeline. In other words, Intel can already offer a US based packaging path at a moment when supply chain resilience and geographic diversification are becoming strategic priorities for large chip buyers.

This is why the EMIB story now looks bigger than a simple Intel comeback narrative. If demand for AI packaging remains stronger than CoWoS supply through 2026, then Intel does not need to displace TSMC across the board to win meaningful business. It only needs to become a credible second lane for customers who cannot wait, cannot secure enough CoWoS capacity, or want more domestic packaging options. Based on Zinsner’s public comments, that shift may already be underway.

There is still an important caveat. The market case for EMIB is becoming stronger, but some of the more specific customer speculation circulating around the story remains just that, speculation. What is firmly supported right now is that TSMC packaging remains constrained, Intel says packaging customer interest is growing fast, and Intel believes some of those packaging deals could scale into the billions annually. That alone makes EMIB one of the more important under watched pieces of the AI infrastructure race heading into the second half of 2026.

If Intel can convert this packaging demand into real volume, EMIB could become one of the clearest examples of how the AI boom is reshaping the semiconductor market beyond GPUs and leading edge nodes. Packaging is no longer a backend detail. It is now a frontline battleground, and Intel may finally have a timely opening.

Do you think Intel’s packaging business can become a serious second pillar for the company, or will TSMC’s CoWoS ecosystem remain too dominant to displace in a meaningful way?