Intel Just Had One Of Its Biggest Earnings Calls Ever, And The Market Finally Noticed

Intel’s Q1 2026 earnings call may become one of the most important turning points in the company’s recent history. After years of pressure around process delays, foundry execution, AI accelerator uncertainty, and intense competition from AMD, NVIDIA, TSMC, and ARM based alternatives, Intel delivered results and guidance that gave investors a reason to believe the turnaround story is gaining real traction.

Intel stock moved sharply higher after the company beat revenue guidance for Q1 2026 and issued stronger guidance for Q2. Foundry and Data Center and AI both showed healthy sequential growth, while Client Computing softened slightly due to inflationary pressure and the ongoing DRAM supply crisis affecting the broader PC market.

Some observers may argue that Intel’s explosive stock reaction was not fully justified by the quarterly numbers alone. However, the real story was not only the revenue beat. The larger signal came from management’s commentary around 18A yields, 14A progress, external customer engagement, AI accelerator strategy, advanced packaging, and Intel’s positioning for agentic AI workloads.

For a company that has spent years asking the market for patience, Q1 2026 sounded less like another promise and more like the early shape of execution.

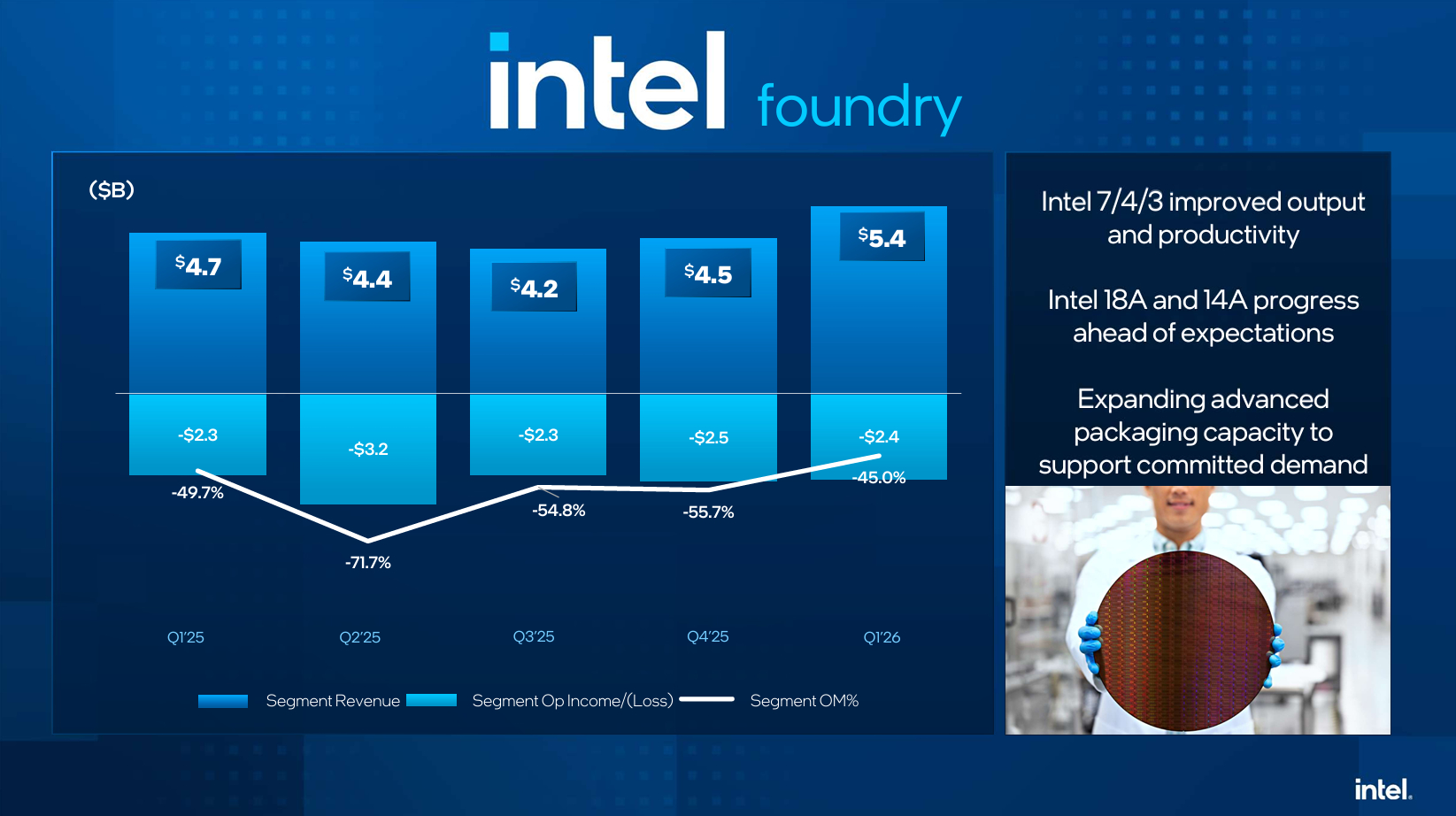

Intel Foundry Shows Real Momentum As 18A Beats Internal Yield Projections

Intel Foundry remains the core of the company’s transformation. The success of Intel 18A is especially important because the node is central to Intel’s product roadmap, external foundry ambitions, and long term manufacturing credibility. Former CEO Pat Gelsinger famously said he had bet the whole company on 18A, and that statement still frames how investors view Intel’s recovery.

During the earnings call, CEO Lip Bu Tan said Intel 18A yields are now running ahead of internal projections, marking what he described as a meaningful improvement in execution and factory output.

"We have made steady progress with Intel 4 and Intel 3, and 18A yields are now running ahead of the internal projections, representing a meaningful inflection in our execution and our factory finished goods output.

Quote by: Lip Bu Tan"

That statement matters because 18A is not just another process node. It is the foundation for a wide range of future Intel products, from entry level platforms such as Wildcat Lake to larger server oriented products such as Clearwater Forest. If Intel can continue improving 18A yields, the company can increase supply, reduce cost pressure, improve product availability, and strengthen confidence among external foundry customers.

For Intel Foundry, yield confidence is everything. Customers do not only want a competitive process on paper. They need predictable production, maturing design kits, manufacturing stability, and evidence that Intel can deliver real products at scale. Beating internal yield ramp projections gives Intel a much stronger case when discussing future commitments with outside customers.

This also helps explain why the market reacted so strongly. Investors were not simply responding to one quarter of revenue. They were reacting to signs that Intel’s manufacturing recovery may finally be entering a more measurable phase.

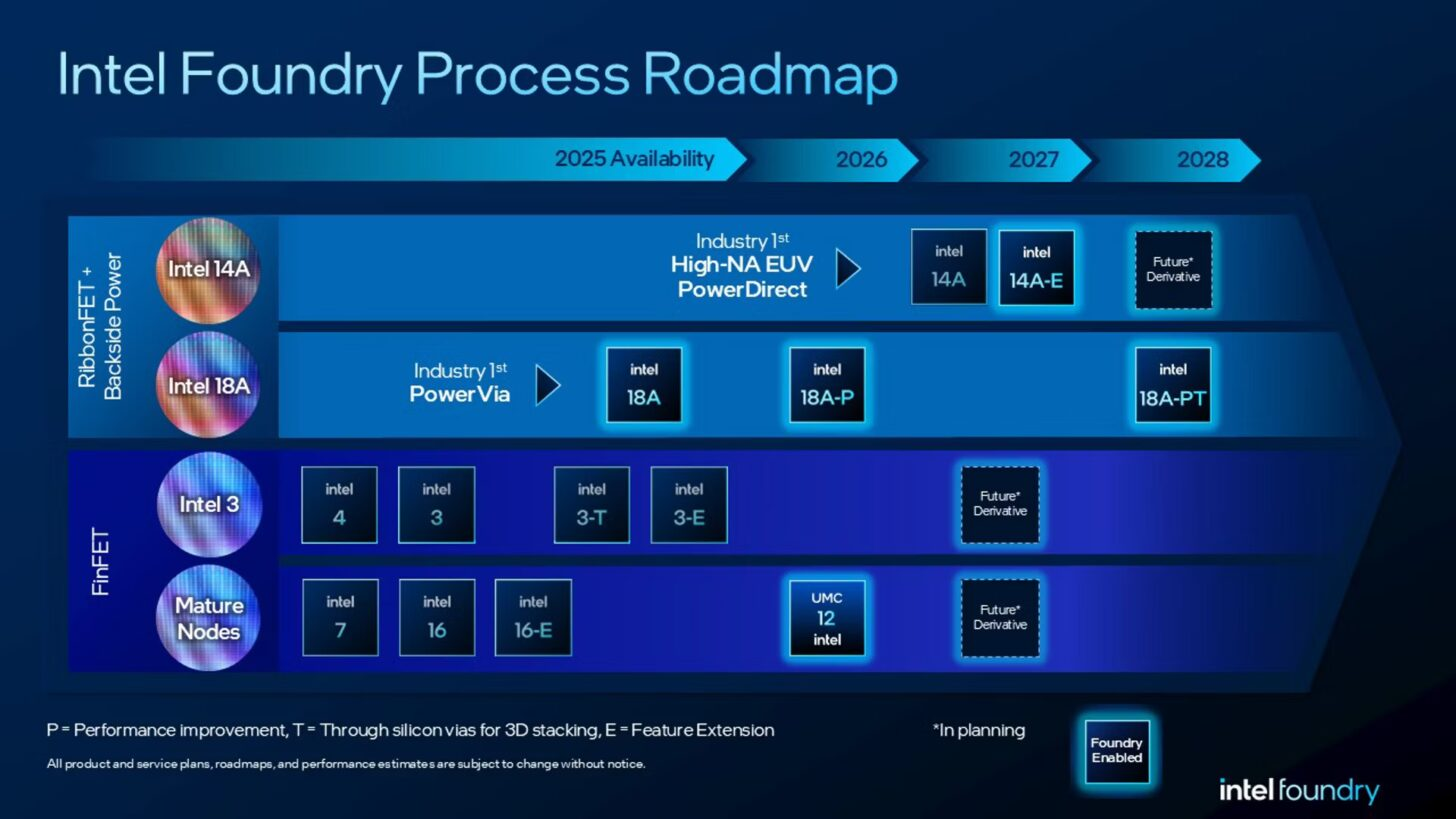

Intel 14A Is Progressing Faster Than 18A At A Similar Stage

Intel’s comments around 14A were just as important. While 18A is the node Intel must execute on now, 14A is the node that could define the next phase of Intel Foundry’s competitiveness. According to Lip Bu Tan, 14A maturity, yield, and performance are already outpacing where 18A was at a similar point in development.

"Intel 14A maturity yield and performance are outpacing Intel 18A at a similar point in time, and we continue to develop PDKs with multiple customers actively evaluating the technology. We expect to see earlier design commitments emerge beginning in the second half of 2026 and expanding into the first half of 2027.

Quote by: Lip Bu Tan"

That is a major confidence signal. Intel has not yet officially confirmed which internal products will use 14A, but high volume Intel product production on the node has been rumored for around H2 2027. If those timelines hold, more details about future Intel products using 14A could arrive soon.

The mention of multiple customers actively evaluating 14A is also critical. Intel Foundry needs external design wins to prove that it can compete not only as an internal manufacturing arm, but as a true foundry alternative to TSMC and Samsung. If customer design commitments begin emerging in H2 2026 and expand into H1 2027, Intel could start building visible momentum in the advanced foundry market.

This is where Intel’s story becomes much larger than CPUs. A successful 14A ramp would support Intel’s broader strategy around advanced packaging, custom silicon, AI accelerators, and chiplet based systems. It could also help customers looking for supply chain diversity during a period of growing geopolitical and capacity concerns in the semiconductor industry.

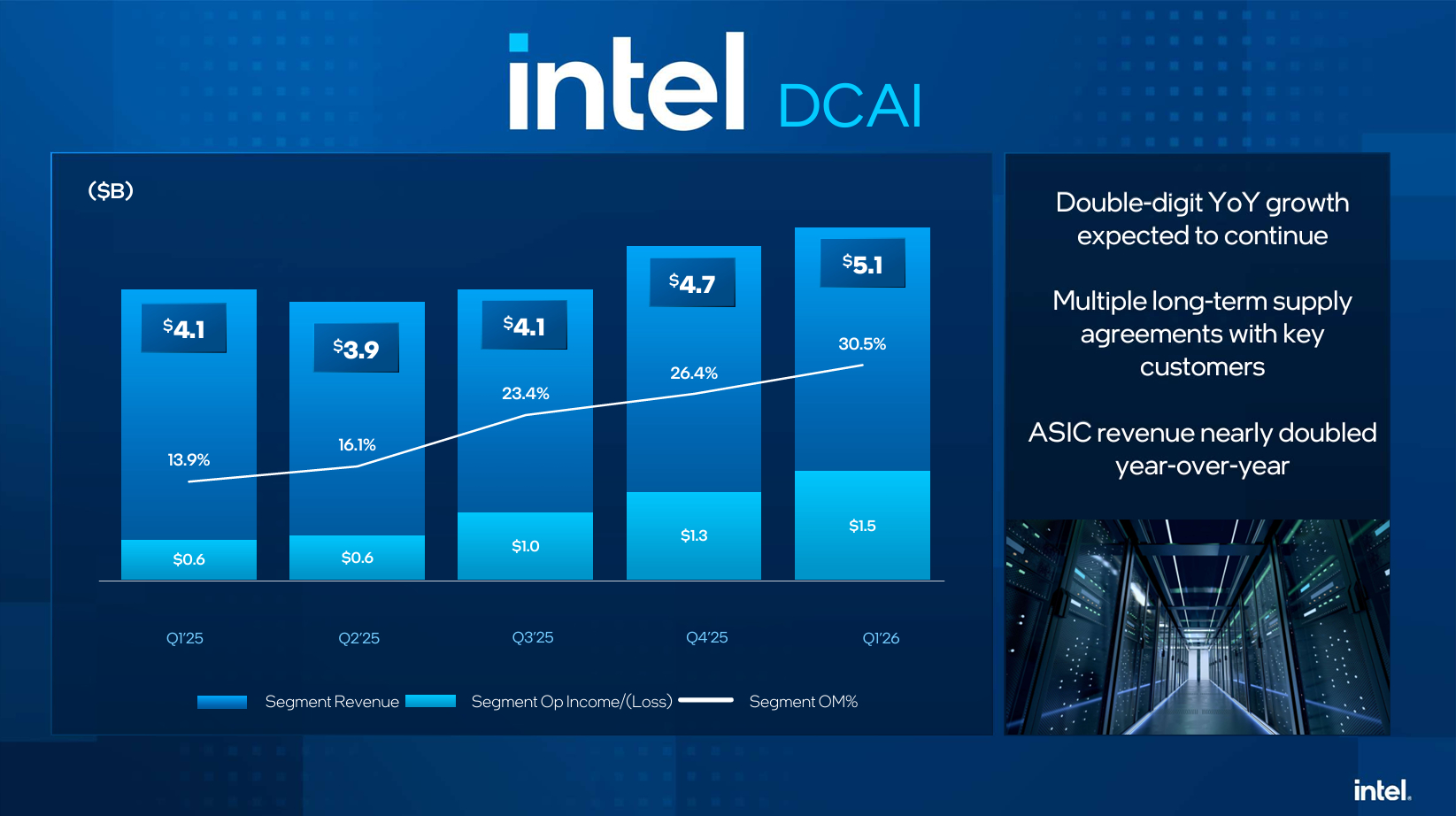

Data Center And AI Strengthen Intel’s XPU Strategy

Intel’s Data Center and AI segment also showed signs of improvement, and Lip Bu Tan used the earnings call to emphasize Intel’s broader competitive advantage beyond traditional CPUs. When asked about Intel’s position against x86 and ARM competitors, he pointed to the company’s ability to combine CPUs, GPUs, accelerators, advanced packaging, and foundry capabilities into what Intel calls XPU solutions.

"The other part is, I think we have a very big advantage with not just the CPU, we have advanced packaging and foundry. I think overall, I think it's exciting time that we call it the XPU. Besides CPU, we're also quietly building up the GPU with a new hire. We are moving into the accelerators, and so that we can serve the customer from the edge and then to the physical AI, and then really drive some of the new initiative to drive the competitiveness.

Quote by: Lip Bu Tan"

This is one of the more important strategic comments from the call. Intel knows it cannot win the AI era with CPUs alone. NVIDIA dominates training and accelerated AI infrastructure, AMD is pushing hard with its Instinct roadmap, and hyperscalers are increasingly building custom silicon. Intel needs a differentiated path, and that path appears to be foundry level integration, advanced packaging, CPUs, GPUs, and accelerators working together.

Intel’s previous AI accelerator roadmap suffered a major setback with Falcon Shores, which was scrapped after failing to meet the company’s strategic needs. Intel then pivoted toward Jaguar Shores, a rack scale solution that remains mostly undisclosed, and Crescent Island, a lower cost accelerator based on Xe3P architecture with 160GB of LPDDR5X memory.

Crescent Island could be interesting for certain inference workloads, but Intel still does not currently have a direct equivalent to AMD’s MI350 or upcoming MI450 class products. That is why Tan’s comment about quietly building up the GPU team is worth watching closely. If Intel is increasing investment in GPUs and accelerators specifically for inference and broader AI deployments, the company may be preparing a stronger competitive push than the market previously expected.

The key question is whether Intel eventually delivers a full scale, HBM equipped accelerator that can compete more directly with AMD and NVIDIA in data center AI. If that happens, Intel’s combination of compute, packaging, and foundry could become a much stronger platform story.

CPUs Could Become More Important In Agentic AI Workloads

One of the most interesting parts of the earnings call came from CFO David Zinsner, who discussed how the CPU to GPU ratio may change as AI moves from training to inference and then into agentic and multi agent workloads.

"If you look at training solutions, they're generally running in the kind of seven to eight GPUs to one CPU. As we look into inference, it's probably getting into the three to four to one kind of level. As you get into agentic and multi agent, it's one potentially even flip in the other direction a little bit. That's one way to think about it. As you think about the growth rate now going forward, it's going to become a significant part of the AI TAM.

Quote by: David Zinsner"

This could become a major opportunity for Intel. Traditional AI training systems are heavily GPU dominated, often with one CPU feeding several GPUs. In inference, the balance begins to shift. In agentic and multi agent workloads, CPUs may become even more important because they can handle orchestration, logic, memory management, control plane tasks, tool calling, scheduling, retrieval operations, and coordination across multiple agents.

If that model scales, future AI infrastructure may not simply be about adding more GPUs. It may require more balanced systems where CPUs play a larger role in managing complex AI workflows. In some cases, CPU demand could rise sharply as enterprises deploy agentic systems that require persistent coordination rather than only raw model execution.

This would be a major shift in AI infrastructure economics. NVIDIA has benefited massively from GPU dominated training and inference demand. However, if agentic AI workloads increase CPU attach rates, Intel could capture a larger portion of the AI total addressable market than many investors currently expect.

This is also where Intel’s packaging and supply chain control become strategically relevant. If customers need tightly integrated CPUs, accelerators, memory, and custom silicon, Intel can potentially offer more than just a chip. It can offer a platform level manufacturing and integration strategy.

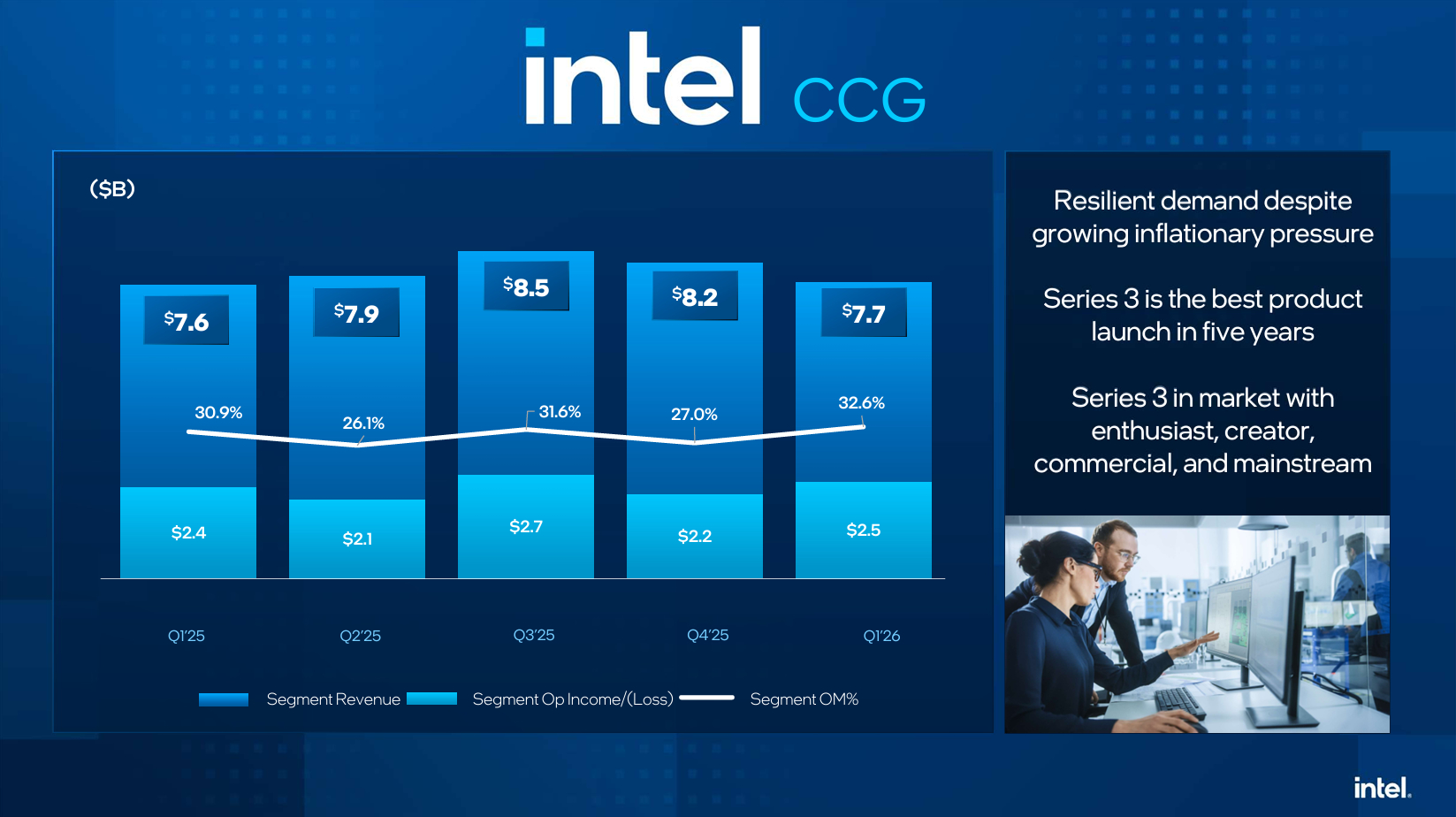

Client Computing Softens But Remains Important

Client Computing was weaker compared with Foundry and DCAI, pressured by inflation and the ongoing DRAM supply crisis. This is not surprising. The PC market remains sensitive to component pricing, consumer spending, and OEM inventory planning. Rising memory costs can affect system pricing and reduce demand, especially in mainstream and entry level segments.

However, Client Computing remains a major pillar for Intel. Even if the segment faces near term pressure, Intel still holds a massive installed base and continues preparing new client products across future process nodes. The success of 18A and future nodes such as 14A will eventually feed into client competitiveness as well.

The bigger issue is that Intel can no longer rely on Client Computing alone to drive investor confidence. The market now wants to see foundry execution, data center growth, AI relevance, and long term process leadership. Q1 2026 helped address those concerns more directly than previous quarters.

The sharp increase in Intel’s stock price may look aggressive if viewed only through the lens of quarterly financials. But the earnings call changed the narrative in several important ways.

Despite the positive tone, Intel’s turnaround is not complete. The company still needs to prove that 18A can scale across products and customers. It must show that 14A can reach production readiness on schedule. It needs to land meaningful external foundry commitments. It needs a stronger accelerator roadmap if it wants to compete more directly in AI. It must also manage cost structure, capital intensity, and customer trust.

The foundry business in particular is brutally difficult. TSMC has years of customer trust, process consistency, ecosystem maturity, and production scale. Samsung remains aggressive. Intel’s technology roadmap may be improving, but external customers will need more than optimism before committing major products to Intel fabs.

Still, the Q1 2026 call suggests Intel is moving in the right direction. More importantly, the company is now giving investors measurable points to track: 18A yields, 14A PDK progress, customer evaluations, design commitments, DCAI growth, and future accelerator announcements.

Intel’s Turnaround Story Finally Has Momentum

Intel’s Q1 2026 earnings call may not prove that the company has fully returned to leadership, but it does suggest that the turnaround is becoming more credible. Foundry execution is improving, 18A is ahead of internal yield expectations, 14A appears to be developing well, and Intel is starting to frame AI as a broader platform opportunity rather than a market it has already missed.

The most important takeaway is that Intel is no longer relying only on promises. The company is beginning to point to execution milestones that can be measured over the next 12 to 18 months. If 18A products launch successfully, if 14A customer commitments emerge in 2026 and 2027, and if Intel can build a more competitive accelerator strategy, the current stock reaction may look less like hype and more like the beginning of a major revaluation.

For now, Intel has done something it badly needed to do: give the market a reason to believe.

Do you think Intel’s Q1 2026 earnings call marks the start of a real comeback, or does the company still need major external foundry wins before investors should fully buy into the turnaround?