Tesla’s 14A Win Gives Intel Foundry a Major Confidence Boost as 18AP and 14A Customer Engagements Expand

Intel’s foundry ambitions have received a major vote of confidence, with CEO Lip Bu Tan confirming that Intel 18AP and Intel 14A are seeing strong external customer engagement. The biggest highlight is Tesla, which has already secured a 14A partnership tied to the broader TeraFab project involving Elon Musk’s companies, including Tesla, SpaceX, and xAI.

For Intel, this is more than a single customer win. It is a strategic milestone for a foundry business that has spent years working to prove it can attract major external partners to its most advanced process technologies. Intel 18A has already been important to the company’s recovery plan, but 18AP and 14A represent the next phase of its roadmap. If Intel can successfully bring these nodes into competitive volume production, the company could regain stronger relevance in the advanced semiconductor manufacturing race.

During Intel’s Q1 2026 earnings call, Lip Bu Tan confirmed the partnership with Elon Musk’s companies to support TeraFab, a project that is expected to use Intel 14A when the process becomes mature enough for production at scale. The 14A node is not yet ready for mass production, but the timing of TeraFab may align with Intel’s process maturity curve, giving Tesla access to Intel’s next generation manufacturing technology when it is ready for larger deployment.

"At a time when advanced wafer capacity is in short supply, this enables us to have better control over our supply chain. Intel has pioneered nearly every major innovation that has enabled dimensional scaling and high volume manufacturing of silicon transistors over the last six decades. We have always been willing to take measured risks that have eventually paved the way for step function improvements in transistor density, cost, power, and performance. As we look to continue challenging the status quo, I can think of no better partner than Elon Musk. We recently announced our partnership with SpaceX, xAI, and Tesla to support TeraFab.

Quote by: Lip Bu Tan"

Elon Musk has also expressed confidence in Intel 14A, describing the process as state of the art. He also acknowledged that 14A is not complete yet, which reflects the current reality of the node. Intel 14A is still in development and is not yet a mature mass production platform. However, by the time TeraFab ramps, Intel expects the node to be in a much stronger position, potentially allowing Tesla to produce future custom silicon using one of Intel’s most advanced manufacturing processes.

This matters because Tesla’s custom silicon strategy is becoming increasingly important. The company is already developing and deploying chips for AI, autonomous driving, robotics, and high performance compute workloads. Tesla has relied on partners such as Samsung and TSMC for chips like AI5, AI6, and AI6.5, but adding Intel as a future advanced manufacturing partner could give the company more flexibility and stronger control over supply.

For Intel, the Tesla win also arrives at an important moment. Advanced wafer capacity remains limited across the industry, and demand for AI silicon, automotive compute, data center accelerators, and custom chips continues to rise. If Intel can prove that 14A is competitive in performance, yield, and cycle time, it could attract more customers looking for alternatives to existing foundry leaders.

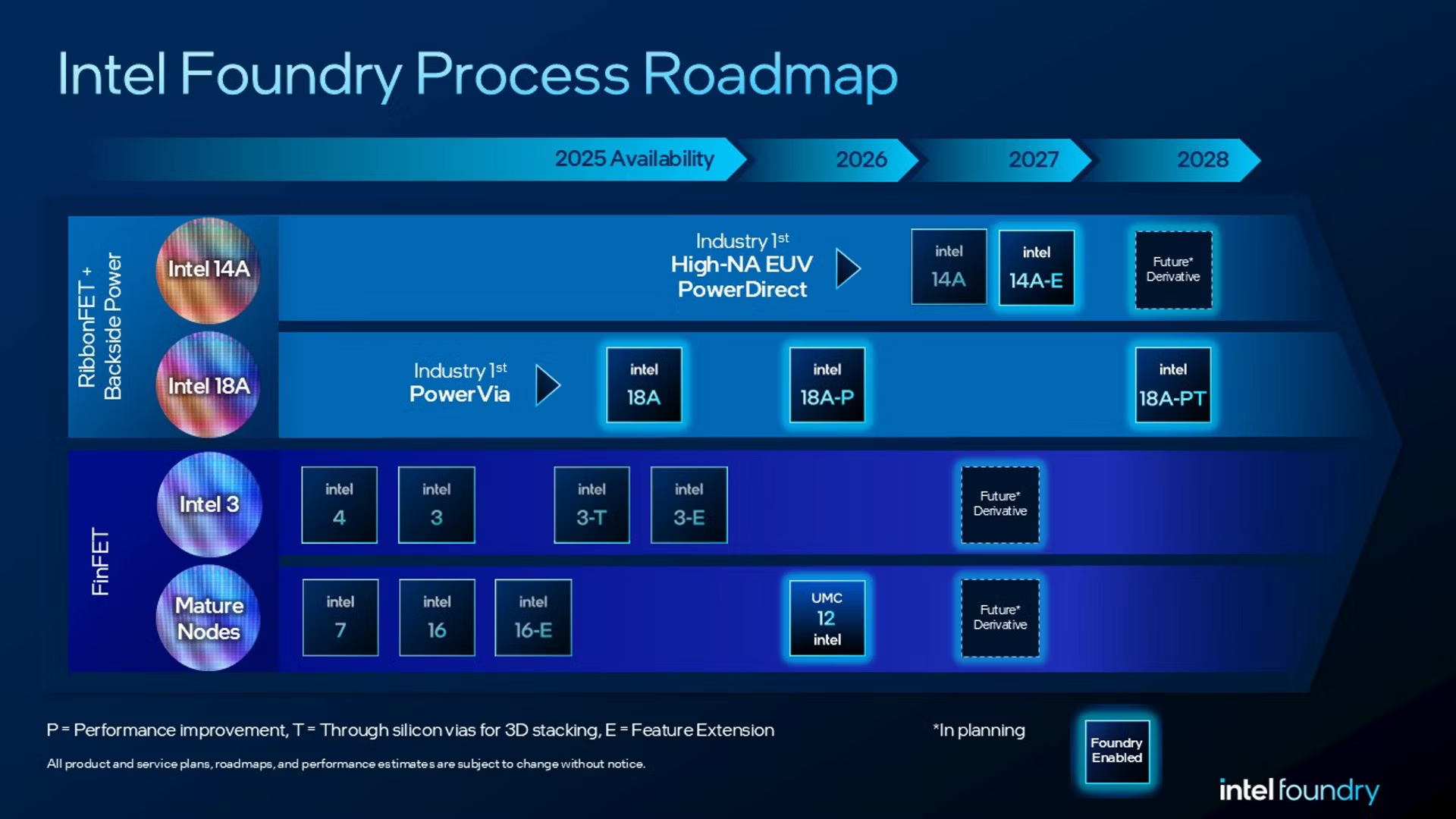

Lip Bu Tan stated that Intel is already encouraged by external engagement on both 18AP and 14A. More importantly, he said that Intel 14A maturity, yield, and performance are already outpacing Intel 18A at a similar stage. That is a significant statement because Intel 18A has been central to Intel’s process recovery story. If 14A is progressing faster and stronger than 18A did at the same point, Intel may have a more competitive foundation for its future foundry roadmap.

"On Intel 18AP and Intel 14A, we continue to be encouraged by our external engagements. Intel 14A maturity, yield, and performance are outpacing Intel 18A at a similar point in time, and we continue to develop PDKs with multiple customers actively evaluating the technology. Their partnership has been critical, and their feedback is continuing to help us define the technology so that we can cater to their needs. We expect to see earlier design commitments emerge beginning in 2026 and expanding into 2027."

Intel is also working toward the next important step for 14A customers: the 0.9 PDK. The company already has the 0.5 PDK available, but the 0.9 PDK is a much more meaningful stage for customer planning. This is where customers begin to make decisions around products, expected volume, and capacity needs. In the foundry business, this stage is critical because it helps transform technical evaluation into actual design commitments.

"On 14A, we already have the 0.5 PDK available and we are aiming for the 0.9 PDK. That is where customers start to decide which products, how much volume, and capacity we need."

Tan also made it clear that Intel does not intend to announce every customer before they are ready to speak publicly. His approach is to let customers reveal their own partnerships when they choose. That is exactly what happened with Tesla, where the customer side moved first before Intel discussed the deal in more detail.

"On 14A, we are making great progress in terms of yield and cycle time, and we are engaging heavily with multiple customers. My style is under promise, over deliver, so we have no plan to announce the customer unless the customer wants to announce it, and we support that. Back to TeraFab, clearly Elon and I believe that global supply is not keeping pace with the rapid acceleration in demand. We both share the vision that we are going to learn a lot together, exploring innovative ways in process and manufacturing. It is a very broad relationship, and we will update you as we go."

The Tesla 14A win is especially important because Intel Foundry needs high profile external customers to validate its long term business strategy. Manufacturing Intel’s own CPUs is one thing. Convincing external companies with demanding silicon roadmaps to commit to Intel’s leading edge nodes is another. Tesla, SpaceX, and xAI represent exactly the kind of high performance, high visibility customers Intel wants to attract.

This also gives Intel a stronger story against TSMC and Samsung. TSMC remains the dominant force in advanced foundry manufacturing, while Samsung continues to fight aggressively for AI, mobile, and custom silicon customers. Intel has the technology ambition, but it needs customer confidence, predictable execution, and proven manufacturing results. Tesla’s involvement gives Intel a powerful credibility boost, especially if more 18AP and 14A engagements turn into actual design commitments between 2026 and 2027.

The broader semiconductor market is also moving in Intel’s favor in one specific area: demand is exploding faster than supply. AI workloads, autonomous systems, robotics, cloud infrastructure, and custom accelerators are all increasing pressure on advanced wafer capacity. If Intel can offer a competitive alternative with 14A, the company could become more attractive to customers that want supply diversity and more control over long term chip production.

Still, the real test will be execution. Intel has made bold foundry promises before, and the market will judge 14A not only by customer announcements, but by yield, performance, power efficiency, design tool readiness, cost structure, and production reliability. A Tesla win is a strong signal, but Intel must now prove that 14A can deliver at the scale and consistency required by customers operating in AI and automotive technology.

For now, Intel has something it urgently needed: momentum. Tesla’s commitment gives 14A a major public validation point, while Lip Bu Tan’s comments suggest more customers are already evaluating Intel’s future nodes. If those engagements mature into design wins, Intel Foundry could begin to look less like an ambitious turnaround project and more like a serious advanced manufacturing contender.

The next key milestone will be the 0.9 PDK for 14A. Once customers begin locking in products, volume, and capacity expectations, Intel’s foundry roadmap will become much easier to measure. Until then, the Tesla deal stands as one of Intel’s most important signals yet that its 18AP and 14A strategy is starting to gain real traction.

Will Tesla’s 14A commitment help Intel Foundry regain trust in advanced chip manufacturing, or does Intel still need more major customer wins before the market fully believes in its comeback?