NVIDIA Blackwell GPUs Double in Price on China’s Black Market as Restrictions Tighten

NVIDIA’s most advanced Blackwell hardware continues to command strong demand in China despite US export controls, stricter customs enforcement, and Beijing’s effort to move domestic technology companies toward locally developed AI accelerators. According to the Financial Times, the price of an NVIDIA DGX B300 system has climbed from approximately RMB 4 million to more than RMB 8 million during the past 6 months, equivalent to around $1.1 million. The same system typically sells for approximately $400,000 in the United States, meaning Chinese buyers are now paying close to 3 times the standard market price through unofficial distribution channels.

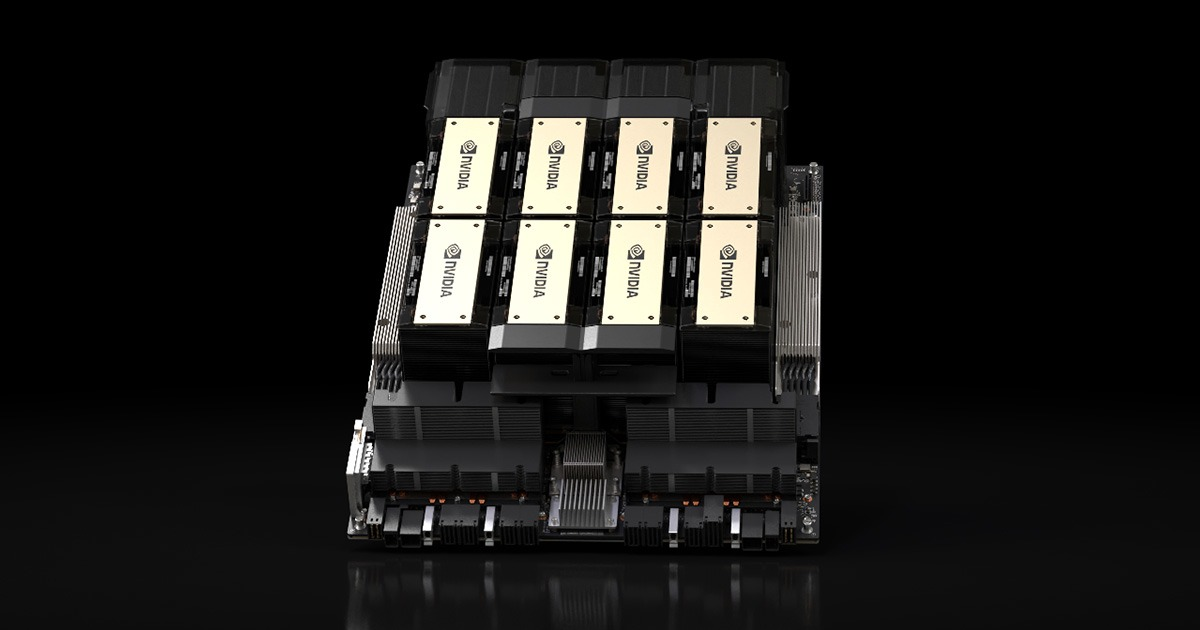

The DGX B300 is a complete artificial intelligence platform rather than a conventional graphics server. According to the official NVIDIA DGX B300 specifications, each system includes 8 Blackwell Ultra GPUs, Intel Xeon 6776P processors, and approximately 2.1 TB of combined GPU memory. NVIDIA designed the platform for large model training, advanced inference, reasoning, and agentic artificial intelligence workloads. The size and complexity of the server make its reported presence inside China particularly notable, since transporting a complete DGX platform requires considerably more coordination than moving individual graphics cards.

Demand has also increased for professional workstation hardware. The NVIDIA RTX PRO 6000 Blackwell has reportedly risen from approximately RMB 50,000 at the beginning of 2026 to as much as RMB 130,000, equivalent to around $20,000. The official NVIDIA RTX PRO 6000 product page lists 96 GB of GDDR7 memory with error correction, 1,792 GB per second of memory bandwidth, and power consumption reaching 600 W. Its 96 GB memory capacity makes it particularly valuable for smaller artificial intelligence companies, research laboratories, and developers that need to operate or fine tune large models without purchasing an entire server platform. This also explains why professional Blackwell cards remain more desirable than consumer products such as the 32 GB GeForce RTX 5090 or the reduced 24 GB RTX 5090 D V2.

US export controls prevent authorized shipments of leading Blackwell products such as the DGX B300 and RTX PRO 6000 Blackwell into China, while also covering other advanced data center accelerators, systems, and consumer graphics cards that exceed defined computing thresholds. However, the regulatory environment does not represent a complete ban on every NVIDIA artificial intelligence processor. In January 2026, the US Bureau of Industry and Security revised its policy for products including the NVIDIA H200 and AMD Instinct MI325X, allowing license applications to be reviewed individually under strict security, testing, supply, and customer requirements. The full conditions are detailed in the official BIS policy update. The H200 uses the older Hopper architecture, but it remains highly capable and continues to outperform many available domestic alternatives.

Chinese technology companies are now operating between 2 opposing policy pressures. Washington is restricting access to advanced American processors, while Beijing is encouraging state funded projects, data centers, and technology companies to prioritize locally produced hardware. Huawei, Alibaba, Biren Technology, MetaX, Moore Threads, and other Chinese semiconductor developers are building processors intended to reduce dependence on NVIDIA. Huawei has emerged as the strongest domestic competitor, its artificial intelligence chip revenue to grow by at least 60% during 2026. However, replacing NVIDIA hardware involves more than selecting another processor. CUDA, optimized libraries, networking products, development tools, system management software, and years of application support continue to make NVIDIA platforms attractive to companies that have already built their infrastructure around the ecosystem.

Migrating a production artificial intelligence operation to domestic hardware may require models, training frameworks, inference engines, monitoring systems, and internal tools to be rewritten or optimized. These technical and financial costs are helping sustain demand for restricted NVIDIA products, including older A100 accelerators and modified gaming graphics cards. The Financial Times reports that Chinese customers are increasingly purchasing a wider selection of older data center and consumer products to compensate for Blackwell shortages, while prices for some older systems have reached approximately RMB 600,000 before stock sells out.

Enforcement is becoming more aggressive as American authorities investigate unauthorized exports and customs agencies across Asia monitor shipments that could ultimately reach restricted Chinese customers. The United States has also clarified that licensing rules can apply to overseas subsidiaries of Chinese companies, reducing opportunities to acquire hardware through regional offices, international data centers, or intermediary businesses. NVIDIA has warned that infrastructure assembled through unauthorized channels may lack warranties, replacement parts, technical support, and verified supply chain documentation, creating substantial operational risks for companies paying premium prices.

The reported price increases show that export controls are making NVIDIA hardware significantly more expensive and difficult to obtain, but they have not eliminated Chinese demand. A DGX B300 selling for more than $1 million reflects severe scarcity and continuing dependence on NVIDIA’s artificial intelligence ecosystem rather than a sustainable supply chain.

China’s domestic semiconductor industry is advancing rapidly, and Huawei is becoming a more credible infrastructure provider, but CUDA remains one of NVIDIA’s strongest competitive advantages. Hardware performance alone does not determine the value of an artificial intelligence platform. Software compatibility, developer familiarity, optimized libraries, networking, documentation, and long term support all influence purchasing decisions.

The likely result is a divided market in which China continues investing in local accelerators while companies with immediate performance requirements search for licensed, cloud based, or unofficial access to NVIDIA technology. For regulators, the central question is whether restrictions are meaningfully slowing development or primarily increasing costs and encouraging more complex procurement networks.

Will stronger export enforcement eventually push Chinese artificial intelligence companies toward domestic chips, or will NVIDIA’s CUDA ecosystem continue driving demand for restricted hardware?