Omdia Warns the PC Industry May Retreat From Budget Devices as Component Shortages Push Vendors Upmarket

The personal computer industry could be heading into a major shift away from affordable systems, and the biggest pressure point appears to be the entry level market. According to a recent Omdia report, the broader US PC market returned to growth in late 2025, but the outlook for 2026 is far more cautious as rising memory and storage costs begin to reshape vendor priorities. Omdia said US PC shipments grew 3% year over year in Q4 2025 to 18.2 million units, but it now forecasts a 13% decline for 2026 as supply constraints tighten across key components.

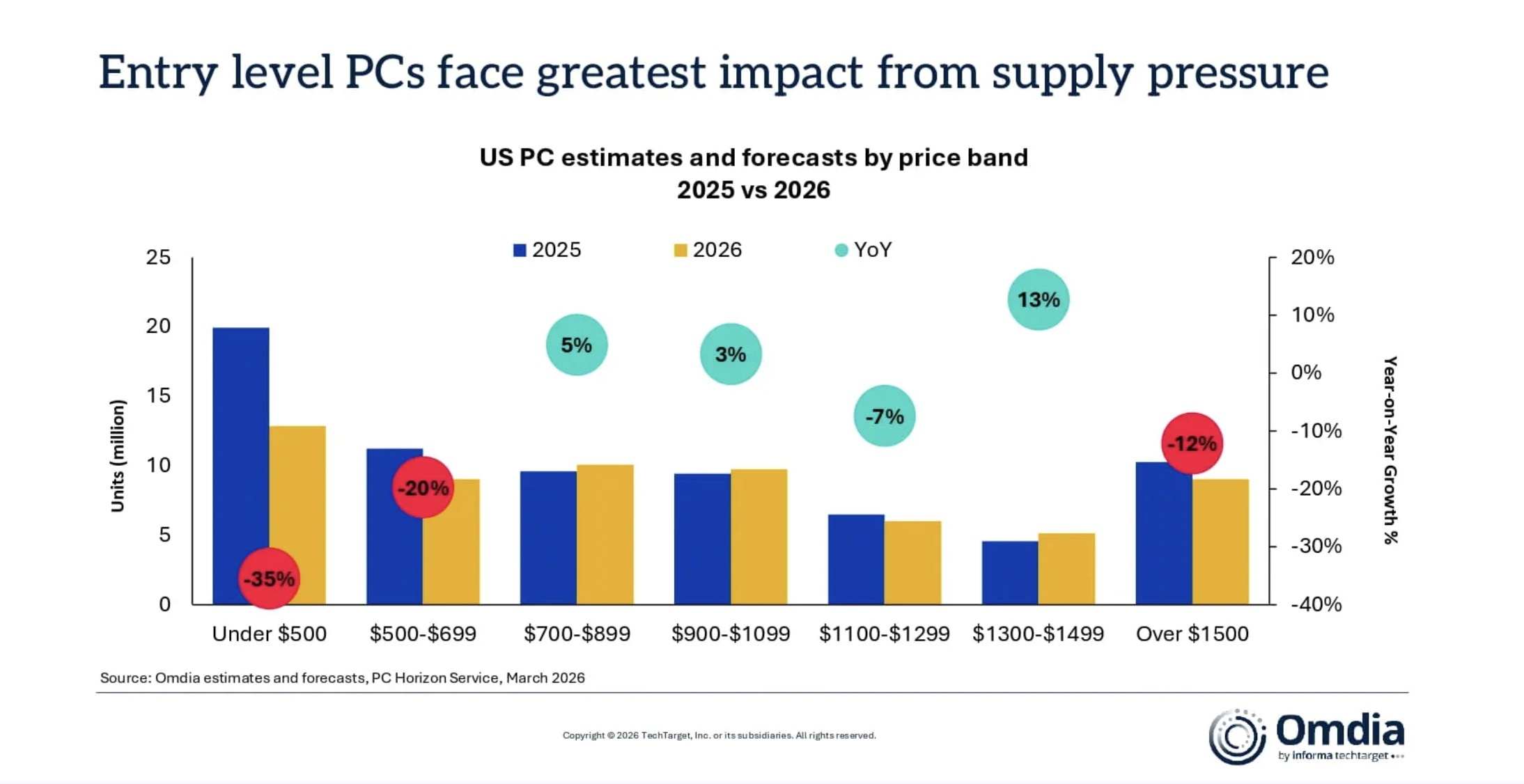

What makes that forecast particularly important is where the pressure is expected to land first. Omdia stated that the sub 500 dollars segment, which covers much of the education market and a large share of entry level consumer devices, is likely to be hit the hardest. In its assessment, thinner margins and lower allocation priority will make it harder for vendors to keep serving the low end profitably, especially when they are being forced to pay much more for core components. Omdia added that smaller vendors could be squeezed the most as a result.

This lines up with the broader concern now moving through the PC supply chain. When the cost of memory and storage rises sharply, low price systems stop making economic sense much faster than premium systems do. Omdia said memory and storage costs had already risen 40% to 70% since the start of 2025, and it expected at least a further 60% increase in mainstream PC memory and storage costs in Q1 2026. Once that kind of inflation hits the bill of materials, vendors naturally start shifting attention toward higher priced devices where they can better protect gross margins.

That means the next phase of the PC market may be defined less by unit growth and more by product mix. Vendors are likely to prioritize notebooks and desktops aimed at buyers willing to spend more, while lower cost education machines and budget consumer systems become harder to source, less attractive to produce, or simply less available at scale. In practical terms, that could mean fewer meaningful options for first time buyers, budget gamers, students, and households looking for a basic low cost upgrade. This is not because demand for those systems disappears, but because the economics behind serving that demand become far less favorable under shortage conditions.

Omdia’s report also suggests that the broader market is already moving in that direction. It noted stronger momentum in premium product lines and pointed to better performance from parts of the market that are less exposed to the margin constraints of entry level hardware. That does not mean the PC space is abandoning mainstream users entirely, but it does suggest the center of gravity is shifting upward. As vendors focus on categories that can better absorb rising component costs, the lowest priced tiers risk becoming the weakest part of the market.

For the industry, the long term concern is that this does not only affect pricing. It also affects accessibility. If the budget segment shrinks significantly, the consequences will be felt across education, entry level gaming, and general consumer adoption. The PC has long remained relevant in part because there was always a wide range of affordable hardware for basic productivity, study, and play. If that layer starts thinning out, the market may become healthier for margin protection in the short term, but narrower in reach over time.

There is also a strategic reason this matters beyond consumer PCs. Many major hardware companies now operate in a market where AI infrastructure, enterprise systems, and premium client devices can all offer stronger upside than low cost consumer machines. As shortages continue, and as suppliers allocate scarce components toward higher value categories, the temptation to deprioritize budget PCs only grows stronger. In that environment, entry level hardware does not just become less profitable. It becomes less important in the eyes of the wider supply chain.

For buyers, that could mean the familiar low cost laptop tier becomes one of the biggest casualties of the current component crunch. For vendors, it may mark the start of a more aggressive upmarket transition. And for the PC industry as a whole, it raises a difficult question about where future growth is supposed to come from if the most accessible end of the market keeps getting pushed aside.

Do you think the PC industry can afford to pull back from budget devices, or will shrinking the entry level segment hurt long term growth and accessibility?