Ex Samsung Chip Boss Says China’s DRAM Expansion Could Ease DDR5 Price Surge by 2027

The global memory market may be heading toward another major shift, as former Samsung Electronics chip executive Kye hyun Kyung believes aggressive investment from Chinese DRAM manufacturers could help cool down current memory prices starting in the second half of next year. His comments arrive at a time when AI demand, HBM allocation, and tight DRAM supply have pushed memory prices sharply higher across consumer, enterprise, and PC hardware markets.

According to Seoul Economic Daily, Kyung, who previously served as the head of Samsung Electronics’ Device Solutions division, shared his outlook during the 285th National Academy of Engineering of Korea Forum. He stated that Chinese memory companies are investing heavily in new production capacity, and if those investments successfully translate into higher output, the additional supply could begin pushing memory prices down around the second half of 2027.

The memory market has been under extreme pressure due to the AI boom. While high performance AI accelerators depend heavily on HBM, the production shift toward HBM has also affected standard DRAM supply. As more wafer capacity is directed toward AI related memory, the availability of conventional DDR5, DDR4, server memory, and consumer PC memory has become tighter. This has created a pricing chain reaction that reaches far beyond data centers.

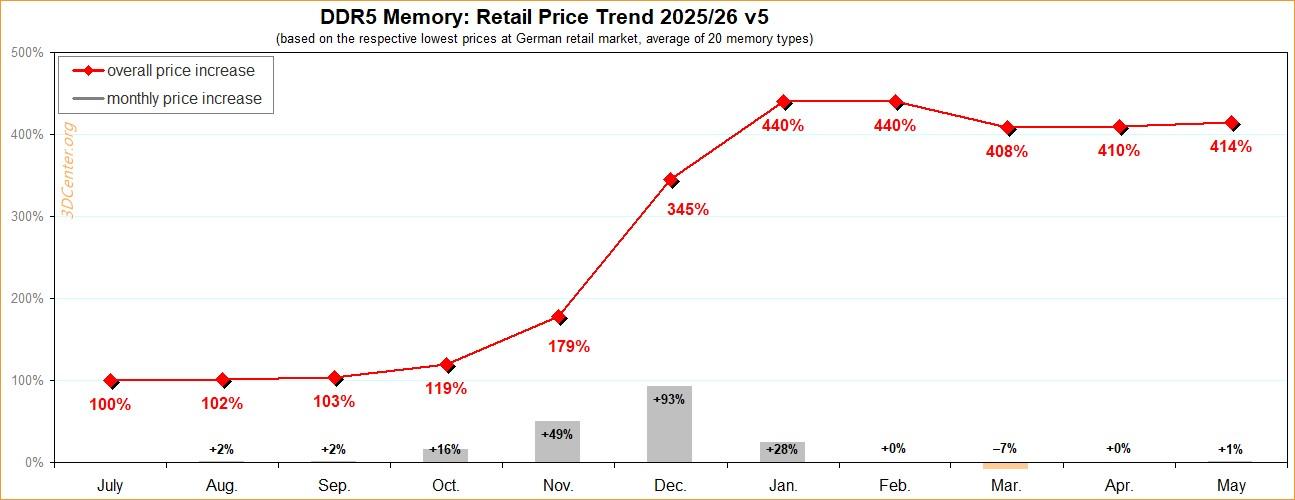

In Germany, DDR5 prices have reportedly climbed by as much as 414% compared with July 2025 levels, showing how aggressively the market has reacted to limited supply and rising demand. The pricing pressure has also affected the broader PC market, with companies such as Apple and Dell reportedly seeing shipment activity influenced by preemptive orders as buyers try to secure systems before higher component prices reach end users. Broader reporting has also linked the memory shortage to AI data center demand and reduced capacity for conventional memory products.

Kyung’s central argument is that China’s aggressive DRAM expansion could eventually reverse part of this pressure. Chinese manufacturers are already moving faster into DDR5 production, with ChangXin Memory Technologies, better known as CXMT, leading the domestic DRAM push. Other Chinese memory related players, including Jiahe Jinwei, are also expanding their role in DDR5 modules and supply chain development.

If China’s investment cycle succeeds, the global memory market could see a meaningful increase in production capacity. Kyung reportedly cited market research data suggesting that total production capacity in the second half of 2027 could reach around 6 million wafers per month. That level of output would have a significant effect on the global supply balance, especially if AI related demand growth slows or if major technology companies begin reducing capital expenditure due to weaker returns on AI infrastructure.

That warning is important. Kyung also cautioned that memory investments depend heavily on whether mega cap technology firms continue seeing strong returns from AI spending. If companies continue building AI data centers aggressively, demand for HBM, DRAM, and NAND may remain strong. However, if AI investment returns weaken, capital expenditure could slow, demand expectations could soften, and the supply side may suddenly become much heavier than expected.

This is the classic risk of the memory industry. DRAM and NAND markets often move through extreme cycles. When demand is high, manufacturers expand capacity. When too much supply arrives at the same time, prices can fall quickly. China’s current expansion could become a stabilizing force for buyers, but it could also create future pressure for established suppliers such as Samsung, SK hynix, and Micron if supply growth outpaces demand.

For South Korea, Kyung’s comments carry a strategic warning. Samsung and SK hynix remain global leaders in advanced memory, especially in HBM and high performance DRAM. However, China’s growing investment in DDR5 and mainstream memory could challenge Korea’s position in more cost sensitive segments. Kyung also argued that Korea needs to expand its presence in fabless chip design to remain competitive with the United States and China.

From a consumer hardware perspective, the possibility of lower memory prices in 2027 would be welcome news. DDR5 pricing has become a major pain point for PC builders, gamers, workstation users, and system integrators. Higher memory prices affect everything from gaming desktops and laptops to AI PCs, mini PCs, handheld gaming systems, and creator workstations. If Chinese DRAM output increases meaningfully, it could help bring more affordable DDR5 kits back into the mainstream market.

However, price recovery will not happen overnight. Even if Chinese manufacturers increase production, the market still needs stable yields, validated products, reliable module partners, and broader platform compatibility. For DDR5 especially, motherboard validation, IC quality, timing consistency, and long term reliability remain critical. Cheaper memory alone will not be enough if the products cannot meet the expectations of OEMs, system builders, and enthusiast users.

For now, the near term outlook remains tight. AI demand continues to dominate memory allocation, HBM remains a high priority product for Samsung, SK hynix, and Micron, and conventional DRAM supply is still under pressure. Several industry forecasts have warned that memory shortages and pricing pressure may persist through 2026 and into 2027, especially if AI server demand remains strong.

The key takeaway from Kyung’s remarks is not that DDR5 prices will immediately collapse. Instead, his view suggests that the market could begin to rebalance in 2027 if China’s DRAM investment produces real volume and if AI capital spending becomes more disciplined. That combination could weaken today’s extreme pricing environment and bring relief to PC hardware buyers, system builders, and memory dependent industries.

China’s DRAM expansion is becoming one of the most important variables in the memory market. If CXMT and other domestic players succeed, the current DDR5 price spike may not last forever. But if AI demand continues to absorb capacity faster than new production can arrive, high prices could remain part of the market for much longer.

What do you think about China’s growing role in DDR5 production? Could CXMT and other Chinese memory makers help bring prices back down, or will AI demand keep DRAM expensive through 2027?