China’s CXMT Pushes Domestic DDR5 Development Forward as Chinese Memory Makers Accelerate Production

Chinese memory manufacturers are moving faster into DDR5 production as the global memory market continues to face supply pressure, pricing volatility, and rising demand from AI, enterprise, gaming, and consumer PC segments. According to the South China Morning Post, domestic module makers in China are accelerating the release of consumer and enterprise memory products powered by DDR5 chips from ChangXin Memory Technologies, better known as CXMT.

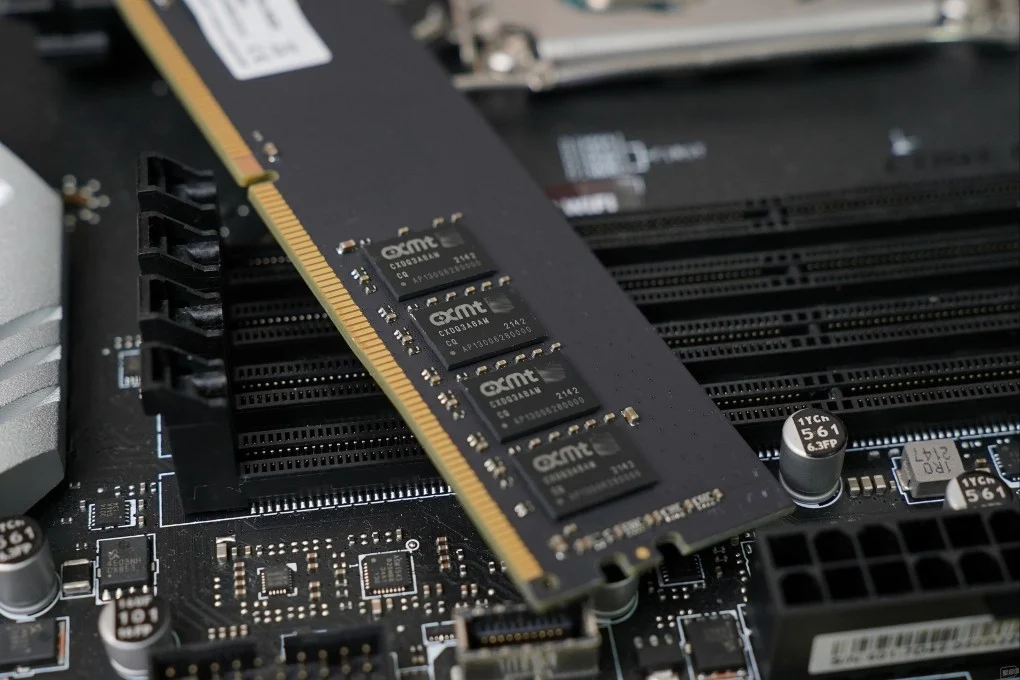

CXMT has become the central player in China’s DRAM strategy, with its latest DDR5 development showing how quickly the company is trying to close the gap with Samsung, SK hynix, and Micron. The market is currently under heavy strain as demand for memory continues to climb, especially with AI servers, workstations, gaming PCs, and high performance computing systems requiring faster and higher capacity modules. This has created an opening for Chinese suppliers to expand their role across both domestic and international supply chains.

The latest development is not limited to CXMT alone. Powev, one of China’s major memory module vendors, has already pushed its Sinker branded DDR5 server memory into mass production and delivery. Its 64 GB DDR5 5600 MT/s RDIMM modules have reportedly passed testing by multiple major customers and are now positioned for enterprise clients, channel partners, and branded vendors. Other Chinese vendors, including Comay, have also released DDR5 products using CXMT dies for industrial and enterprise applications.

For the consumer market, Chinese made DDR5 modules have been moving beyond prototype stage since 2024, with Powev’s Gloway and KingBank DDR5 models based on domestic DRAM chips already appearing in commercial channels. This shows that China’s DDR5 ecosystem is no longer only focused on limited demonstration products, but is now moving toward broader availability for mainstream users and system builders.

CXMT officially introduced its DDR5 product portfolio in November 2025, with chips supporting speeds up to 8000 MT/s and die densities of 16Gb and 24Gb. These chips target servers, workstations, and personal computers, giving Chinese module makers a more competitive domestic foundation for next generation memory products. While the most advanced global suppliers have already moved into 32Gb DDR5 dies, CXMT’s 16Gb and 24Gb progress still represents a major step for China’s memory ambitions.

The broader market context is also working in CXMT’s favor. Reuters reported that CXMT expects first half 2026 revenue to reach between 110 billion yuan and 120 billion yuan, equal to about 17.62 billion dollars, as global DRAM demand continues to exceed supply. CXMT also reported that its first quarter revenue jumped more than 700% year over year to 50.8 billion yuan, supported by higher DRAM prices, stronger output, and an improved product mix.

This rapid growth comes as the global memory industry remains concentrated around Samsung, SK hynix, and Micron. Reuters previously reported that CXMT held around 4% of the global DRAM market in Q2 2025, while the 3 leading suppliers controlled more than 90% combined. CXMT is also seeking to raise 29.5 billion yuan, equal to about 4.22 billion dollars, through a Shanghai listing to upgrade production lines, advance DRAM technology, and expand its future product roadmap.

The policy environment around Chinese memory makers remains fluid. While some reports have pointed to changing United States treatment of CXMT and YMTC, the situation should not be framed as a simple full removal of restrictions. Reuters reported in February 2026 that an updated Pentagon list was briefly published and then withdrawn, and that the withdrawn version had removed CXMT and YMTC from the list. The report also noted that the reason for the withdrawal was unclear and that some removals appeared to still be under review.

Samsung’s shift away from older LPDDR standards has also created an opportunity for Chinese DRAM suppliers. As larger memory makers focus more capacity on advanced products and AI related memory, Chinese suppliers have room to expand LPDDR4 and mainstream DRAM output for entry level smartphones, PCs, and other cost sensitive devices.

For the gaming and PC hardware market, this could eventually mean more DDR5 options across different price segments. If Chinese suppliers continue scaling production and improving validation, users may see more affordable memory kits in the future, especially in markets where pricing, supply, and trade costs have made DDR5 upgrades more expensive. However, performance consistency, platform compatibility, long term reliability, and motherboard validation will remain key factors before these products can fully compete with established global brands.

CXMT’s DDR5 push is more than a domestic milestone. It reflects a wider shift in the memory market, where AI demand, supply constraints, pricing pressure, and geopolitical factors are reshaping how DRAM is produced, sourced, and adopted. The next stage will depend on how fast Chinese memory makers can scale volume, improve yields, validate higher speed modules, and gain trust across enterprise, consumer, and enthusiast platforms.

What do you think about China’s rapid DDR5 progress? Could CXMT become a serious global challenger to Samsung, SK hynix, and Micron, or will validation and ecosystem trust remain the biggest obstacles?